New Zealand Foreign Trusts articles

Date

19 Jun 2023

Related Expertise

1. New Zealand as a Virtual Business Centre – Foreign Trusts

1.1 New Zealand is gaining attention as a favorable location for nominal business ownership due to some not well-known factors. In today’s uncertain world, with factors such as Brexit, EU instability, Eastern

European risks, US/China trade wars, and ongoing issues with North Korea etc, New Zealand stands

out as a stable option. It offers political, financial, legal, and social stability, with a robust legal system

and international copyright adoption. This stability is attracting interest in foreign trusts based in New

Zealand.

2. Offshore Business Ownership Problems

2.1 Scenario: A company currently operates in an overseas jurisdiction. Its parent company (or it could be a Foundation, Family Office or High Net Worth Individual – all these will be referred to as ‘Parent Company’) to which the company pays profits through dividends or returns such as royalties, IP rental or interest, could be in the same jurisdiction or in another jurisdiction, possibly in a low-tax or tax haven country.

2.2 Currently, if the company has its Parent Company in places like Bahamas, BVI, Marshall Islands and Vanuatu etc. in it is becoming increasingly difficult (if not already impossible) to transact business with the EU and the US who are putting more and more pressure on such low or no-tax countries as well as concentrating on the Parent Company and its Ultimate Beneficial Ownership (UBO) for tax avoidance or evasion. [For example, the EU countries and defensive measures taken against them are listed here EU list of non-cooperative jurisdictions for tax purposes – Consilium (europa.eu) ]

2.3 It is becoming increasingly challenging, and sometimes impossible, to carry out fund transfers with some jurisdictions due to reasons such as Anti-Money Laundering (AML) and Counter Financing of Terrorism (CFT). Banks are growing more cautious when dealing with companies located in countries considered to be in a grey or blacklist jurisdiction. Association with such countries can negatively impact business counterparty confidence, affecting cross-border payment transactions and compliance with regulations like FATCA.

In summary, the jurisdiction of the Parent Company in many jurisdictions is becoming a major concern for business owners globally.

3. New Zealand Foreign Trust Benefits and Comparisons and Structure

3.1 However, if the Parent Company jurisdiction was New Zealand, these difficulties are solved. New Zealand provides a Parent Company with advantages that are not available in other jurisdictions such

as the UK, EU countries, the US or Australia. A principal difference is that, unlike these other countries, income passing through New Zealand qualifying exempt foreign trusts will not be taxed in New Zealand.

3.2 Even if the issues related to offshore business ownership don’t affect a Parent Company, opting for New Zealand “ownership” can enhance business credibility without compromising existing arrangements. Following the Panama Papers scandal, New Zealand’s foreign trust regulation has gained approval from the OECD, making it the only country worldwide with this distinction. Additionally, New Zealand is considered a “white-list” country. By registering in New Zealand, businesses benefit from being associated with an established, stable, and developed nation, free from any negative elements such as a reputation for money laundering or foreign corrupt practices, political instability, financial volatility, or social unrest. This provides reassurance to banks, suppliers, customers, and others involved in business dealings.

3.3 Furthermore, NZ registration affords some protection from regulatory changes that may be more likely in other jurisdictions. For instance, the UK faces uncertainties and necessary adjustments resulting from Brexit, while other European countries may encounter changes imposed by the EU.

3.4 Relocation of the Parent Company to New Zealand does not change the location of the business or any aspects of the activities of the operating company. And, depending upon the tax requirements of the operating company’s jurisdiction, there may very well be additional advantages including from tax arbitrage.

3.5 We recently received a direct proposal from an overseas business who explained why they were opening an operation in NZ (although not strictly for virtual jurisdiction reasons but for largely transacting overseas) this way:

(a) It is English-speaking, and its legal system is governed by the general principles of Common Law.

‘New Zealand enjoys a number of significant advantages:

(b) It is widely perceived as a corruption-free, politically and economically stable environment for conducting business.

(c) The regulatory regime governing the provision of financial services enjoys an excellent international reputation, particularly as it relates to the implementation of FATF best-practice standards.

(d) While it is not the ideal location in terms of time zone coordination, it does enjoy a “first up, best dressed” advantage, in that the New Zealand working day can incorporate the start of trading on Australasian, South-East Asian and Chinese markets. With a few hours of overtime, or by delaying the start of business to mid-morning, it can also do the same for European markets.

(e) New Zealand’s telecommunications and banking infrastructure is highly developed, meaning that both information and capital can be rapidly deployed, resulting in a low-friction trading environment.

(f) The cost of establishing the infrastructure and human resources base, and obtaining the regulatory approval, necessary to operate a [business description] business is relatively low when compared with alternative jurisdictions we considered’.

Of course “time zone coordination” is not an issue for a virtual jurisdiction.

4. New Zealand Foreign Trust Structure and Requirements

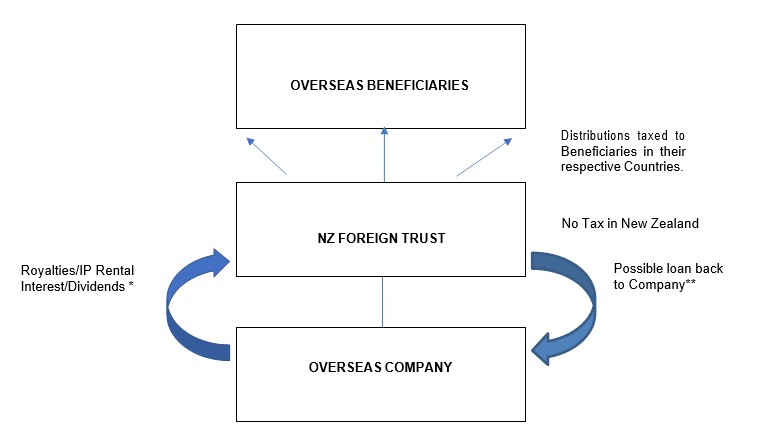

4.1. A structure could look like this:

** Foreign Trust – Owned assets (e.g. IP) could be leased back to create income for Beneficiaries but, depending upon the relevant tax jurisdiction, with rental/royalty/interest payments often tax-deductible to the operating company.

4.2 A qualifying (that is, meeting the requirements to qualify as a ‘foreign trust’ under New Zealand tax law) foreign trust (Trust) must have the following:

(a) a New Zealand-resident Trustee. This will be a New Zealand company with an NZ-based director (which we can provide in association with our accounting partner);

(b) income that is not derived (or deemed derived) from New Zealand;

(c) no New Zealand-resident settlors (people who have contributed assets to the Trust);

(d) no New Zealand-resident beneficiaries;

If the Trust meets these requirements the foreign income earned by the Trust will be exempt from New Zealand income tax and will be able to be passed back to the UBO without deduction in New Zealand.

4.3 New Zealand’s regulatory systems are highly digitalized, allowing for easy access and transactions from anywhere in the world. Company records, legislation, and even land titles can be accessed and processed electronically. This efficient system enables companies to be incorporated ‘same day’, sometimes within a matter of hours. Remote operations for activities such as banking and land transactions are also possible. As a result, New Zealand has achieved a high global ranking for ease of doing business. For more information, refer to our informational sheet titled “New Zealand as a Business Centre for Investment in New Zealand” and the Ease of Doing Business in New Zealand – 2022 Data – 2023 Forecast on tradingeconomics.com.

5. New Zealand Foreign Trust Disclosure Rules

5.1 Once the foreign Trust is properly set up to effectively allow income to pass through to the overseas beneficiaries New Zealand-tax free, the Trusts will then need to comply with recently enacted disclosure requirements:

(a) Each foreign trust must be registered with the New Zealand Inland Revenue Department (IRD) with information including details of settlors (not only named settlors under the Trust Deed but also deemed settlors such as anyone settling, providing benefits to or transferring assets to the Trust) and overseas beneficiaries under the Trust Deed. New foreign trusts must register within 30 days. The registration fee is NZ$270.

(b) After registration, each foreign Trust must file an Annual Return which includes the Trust’s financial statements and details of settlements and distributions made over the relevant year. The Annual Return must also include any changes made to the information that was provided as part of the initial disclosure on registration (for example, additional settlors or beneficiaries or changes to them). Accordingly, the financial information effectively only tracks Trust inputs and outputs (settlements and income receipts and distributions) to ensure they match the tax free requirements. The annual filing fee for the annual return is NZ$50.

(c) The IRD reserves the right to information share with other agencies including the New Zealand Police and relevant government departments. As for information sharing with foreign governments or agencies, New Zealand is a participant in the Common Reporting Standard (CRS) protocol. It may share information with a foreign jurisdiction if that jurisdiction has an AEQI (Automatic Exchange of Information) relationship with New Zealand. For further information on this the IRD has general information on CRS and AEOI on their website: https://www.ird.govt.nz/international/exchange/crs/aeoi-crs/.

(d) Nevertheless, the IRD is obligated to keep the information confidential, as it is required to do for all taxpayers. In the case of a New Zealand-resident trustee company, the shareholders and director(s) would also be residents of New Zealand, ensuring that there is no public scrutiny of the settlors or beneficiaries at that level either. Thus, only the New Zealand government and possibly overseas agencies would have knowledge of the identity of the settlers and beneficiaries.

We are happy to discuss requirements or provide further information on New Zealand foreign trusts.

About Stace Hammond

The Stace Hammond Firm is 111 years old. Stace Hammond specialises in Corporate, Business and Bank and Finance related legal advice including Business Structuring, Mergers and Acquisitions, Structured Finance, Public Offers & Securities, Private Equity, Venture Capital and Managed Funds, Foreign Investment and Intellectual and Real Property legal advice and commercial litigation.

Subscribe

Get insights sent direct to your email.